Blank Pennsylvania Petition Template

PA Documents Online

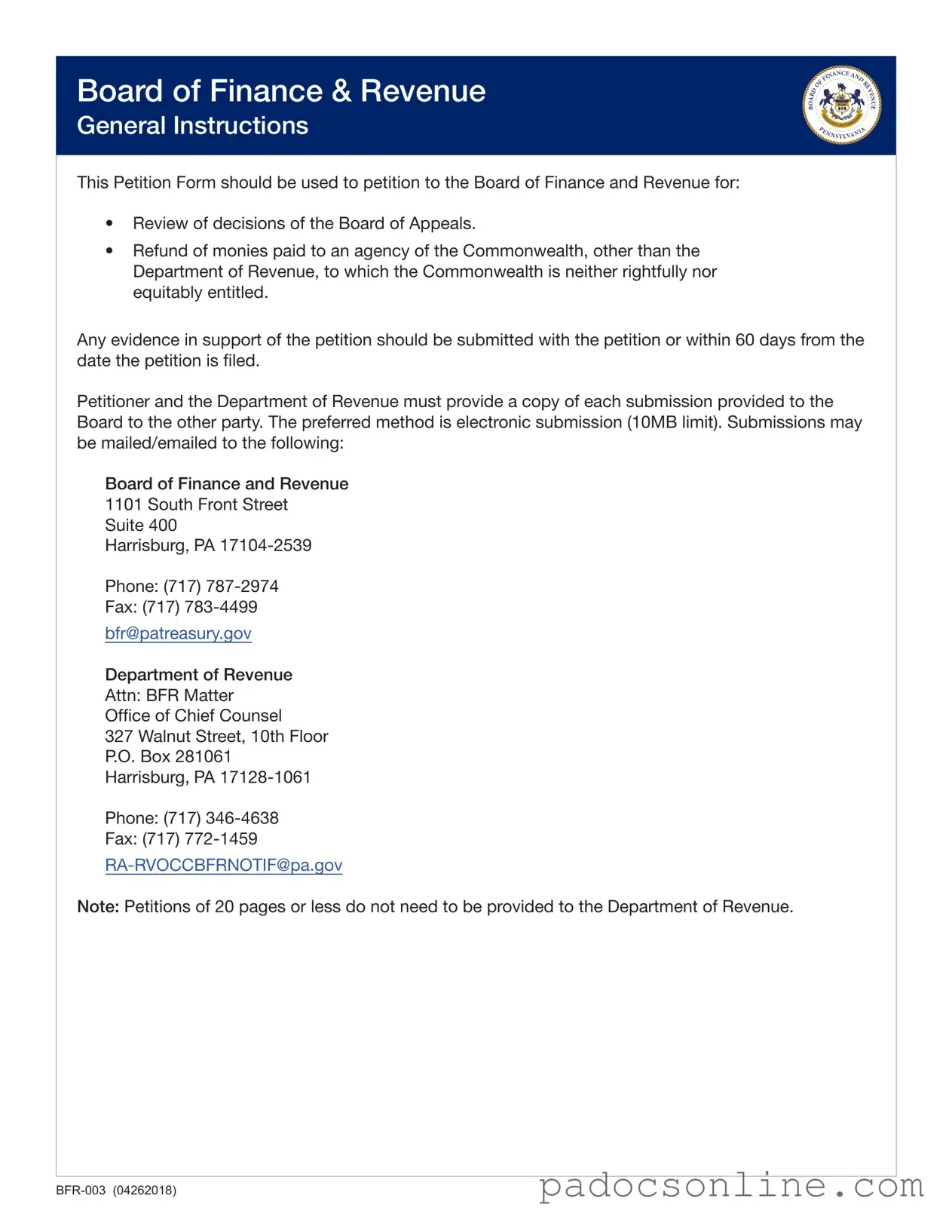

Blank Pennsylvania Petition Template

When filling out the Pennsylvania Petition form, it is important to follow certain guidelines to ensure the process runs smoothly. Below is a list of things you should and shouldn't do.

Can a Felon Hunt in Pa - The final decision on your challenge will be issued within 60 days of receipt.

The CDC U.S. Standard Certificate of Live Birth form is an essential document used to officially record the details of a newborn's birth in the United States. This standardized form plays a critical role in public health, legal identity, and statistical record-keeping. New parents can find useful resources and templates related to this form at freebusinessforms.org, which can help them navigate the important steps following the arrival of their little ones.

Pennsylvania Tax Forms - Signing the petition is mandatory for all submissions.

Filling out the Pennsylvania Petition form can be a straightforward process, but there are several common mistakes that people often make. Recognizing these errors can save time and prevent delays in the resolution of your case. One frequent mistake is failing to include the Board of Appeals Docket Number when available. This number is crucial for identifying your case and ensuring that it is processed correctly.

Another common error is not completing all required information. Each section of the form must be filled out accurately. If the petitioner is an organization rather than an individual, it is essential to include a contact person. Omitting this detail can lead to confusion and miscommunication.

Many people neglect to indicate if they intend to be represented by someone else. This step is important because it determines where all correspondence will be sent. If a representative is chosen, the petitioner must ensure that the representative’s information is provided clearly on the form.

In section four, some petitioners forget to specify the tax amount they are appealing. This information is vital, as it helps the Board understand the financial implications of the petition. Additionally, checking the appropriate box to indicate the type of petition is essential for proper categorization.

When it comes to hearings, it is important to note that they are held in specific locations. Petitioner requests for hearings should be made clear, as failure to do so may result in a decision being made without a hearing. If a compromise is desired, the appropriate box must be checked, and the Request for Compromise Form needs to be submitted within the specified timeframe.

Another mistake involves signatures. All petitions must be signed by the petitioner or an authorized representative. A missing signature can lead to immediate rejection of the petition. Furthermore, the affidavit section must be completed honestly, affirming that the information provided is accurate and not intended for delay.

Providing insufficient details about the relief requested is also a common pitfall. The petition should clearly state the basis for the request, including all pertinent facts and relevant calculations. Supporting evidence must be included with the petition or submitted within the allowed timeframe. Late submissions may not be considered.

Lastly, failing to attach necessary documentation can significantly weaken a petition. For instance, when appealing sales and use tax, including the audit or assessment is crucial. Similarly, if appealing personal income tax, attaching the PA-40 and relevant schedules is essential for a thorough review.

By being aware of these common mistakes, petitioners can improve their chances of a smooth and efficient process. Attention to detail is key, and ensuring all sections are completed accurately will facilitate a quicker resolution of the petition.