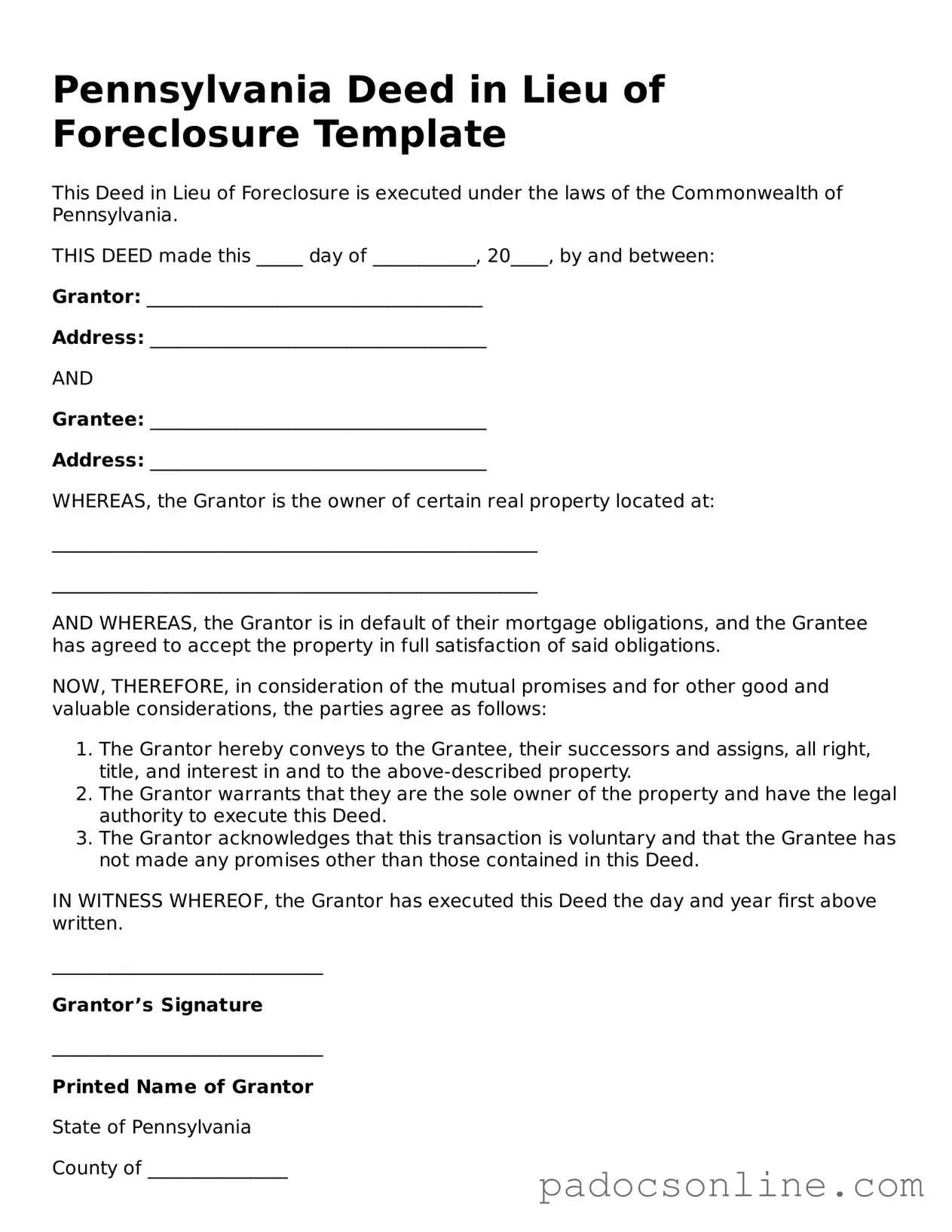

Legal Deed in Lieu of Foreclosure Document for the State of Pennsylvania

PA Documents Online

Legal Deed in Lieu of Foreclosure Document for the State of Pennsylvania

When filling out the Pennsylvania Deed in Lieu of Foreclosure form, it is essential to follow certain guidelines to ensure the process goes smoothly. Here are ten things to keep in mind:

Letter of Intent to Homeschool Colorado - Informs the school district of a child’s homeschooling status.

The Illinois Quitclaim Deed form serves as a legal instrument to transfer ownership of real property from one party to another, without warranties regarding the title's quality. This simplified conveyance process does not guarantee the grantor holds clear title, making it a common tool for transactions among trusted parties, such as family transfers or divorces. For those looking to proceed, the form can be filled out by clicking the button below. Additionally, you can find more information and resources by visiting All Illinois Forms.

Power of Attorney for Car Title - When filled out correctly, this form is a legal instrument recognized by authorities for vehicle transactions.

Filling out and using the Pennsylvania Deed in Lieu of Foreclosure form involves several important considerations. Here are key takeaways to keep in mind:

Filling out the Pennsylvania Deed in Lieu of Foreclosure form can be a daunting task. Many individuals encounter pitfalls that can lead to complications down the line. One common mistake is failing to provide accurate property information. It’s crucial to ensure that the address and legal description of the property are correct. Errors in this section can cause delays or even invalidate the deed.

Another frequent error is neglecting to sign the document. A deed in lieu must be signed by all parties involved. Without the necessary signatures, the deed cannot be processed. It’s important to double-check that every required signature is present before submitting the form.

People often overlook the need for notarization. In Pennsylvania, the deed must be notarized to be legally binding. Failing to have the document notarized can lead to issues when attempting to transfer ownership. Make sure to schedule a meeting with a notary public to complete this step properly.

In addition, some individuals do not fully understand the implications of the deed in lieu. They may mistakenly believe it absolves them of all liabilities related to the property. While it can relieve some financial burdens, it’s essential to consult with a legal professional to grasp the full scope of responsibilities that may still exist.

Another mistake involves not providing the necessary supporting documentation. Lenders may require additional paperwork to process the deed. This could include proof of hardship or other financial documents. Gathering all required materials upfront can streamline the process and prevent delays.

Furthermore, individuals sometimes fail to communicate with their lender. Open lines of communication are vital. Not informing the lender about the intent to execute a deed in lieu may lead to misunderstandings or complications. Keeping the lender in the loop can help facilitate a smoother transaction.

Finally, some people underestimate the importance of reviewing the completed form. Before submitting, it’s wise to carefully read through the entire document. This review can help catch any mistakes or omissions that could cause problems later. Taking the time to ensure accuracy can save significant headaches in the future.